The two World Wars did more than devastate nations and claim tens of millions of lives. They dismantled the economic foundations of the old world and forced the construction of an entirely new global system. Before the twentieth century, wealth and power were still largely rooted in land, empires, and colonial extraction. By the time the wars ended, economic dominance depended on industrial capacity, financial control, technological innovation, and the ability to coordinate entire societies under pressure.

World War I shattered long-standing financial norms, collapsed empires, and exposed the fragility of gold-based monetary systems. World War II went even further, transforming governments into economic managers, accelerating industrial production to unprecedented levels, and permanently shifting the balance of power away from Europe toward the United States. Together, the wars did not merely interrupt global trade; they rewrote the rules by which economies functioned.

This article examines how total war forced governments to mobilize labor, capital, and technology on a scale never seen before, how financial systems broke and were rebuilt, and how new global institutions emerged to prevent another collapse. It explores the long-term economic consequences that followed—rising state intervention, the birth of the modern middle class, the decline of empires, and the emergence of a globalized economy shaped by strategic planning rather than tradition.

Understanding how the World Wars transformed the global economy is essential to understanding the modern world itself. Many of today’s financial structures, labor systems, and international institutions exist not despite those conflicts, but because of them.

1. The Pre-War Global Economy: A Fragile Balance of Empires

Before World War I, the global economy was dominated by European empires. Britain, France, Germany, and others controlled vast colonial networks that supplied raw materials and consumed manufactured goods. Trade routes were stable, currencies were often tied to gold, and international finance revolved around a few major capitals.

This system looked strong, but it was fragile. It depended on:

-

Colonial exploitation

-

Stable political alliances

-

Limited government intervention

-

Faith in gold-backed currencies

Industrialization had increased productivity, but wealth was unevenly distributed. Many economies were deeply interdependent, meaning disruption in one region could ripple globally. When war arrived, this tightly connected system proved unable to absorb the shock.

2. World War I: Economic Mobilization on an Unprecedented Scale

World War I forced governments to take direct control of their economies in ways never seen before. Total war required total mobilization.

States redirected factories from consumer goods to weapons and ammunition. Governments fixed prices, controlled wages, rationed food, and dictated production priorities. Entire industries became extensions of the military.

To fund the war, countries abandoned traditional fiscal restraint. They borrowed heavily, raised taxes, and printed money. Gold standards were suspended, breaking the link between currency and precious metals. Inflation followed, especially in countries that lost the war.

The war demonstrated something revolutionary: governments could centrally manage economies during emergencies. This idea did not disappear when the fighting stopped.

3. Debt, Inflation, and the Collapse of Old Financial Systems

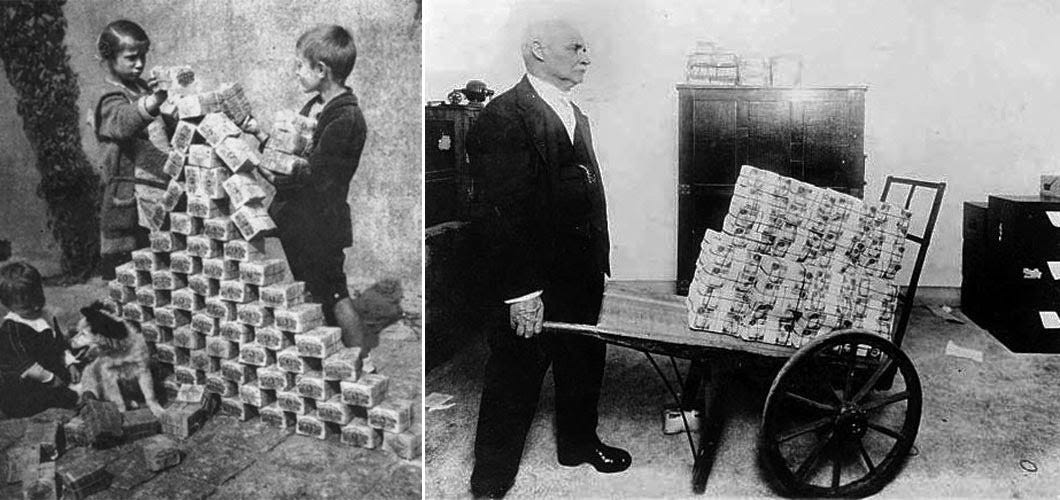

The financial aftermath of World War I was catastrophic. European economies were drained, indebted, and unstable.

Germany faced massive reparations that crippled its economy. Hyperinflation wiped out savings and destroyed trust in money itself. Austria, Hungary, and other former empires experienced similar collapses as political borders shifted and markets fractured.

Britain and France emerged victorious but financially weakened. They owed enormous debts to the United States, which had become the world’s main creditor almost overnight.

The global financial center shifted from London to New York. Capital, investment, and monetary influence followed. This marked the beginning of American financial dominance.

4. Labor, Society, and the Economic Role of the State

World War I permanently changed labor markets and social expectations.

With millions of men at the front, women entered factories, offices, and heavy industry in unprecedented numbers. This was not temporary in impact, even if many women were pushed out afterward. The idea that labor roles were fixed by gender was permanently weakened.

Governments also expanded welfare measures to maintain morale and productivity. Pensions, unemployment support, and healthcare programs grew out of wartime necessity.

The relationship between citizens and the state changed. Economic security was no longer seen as purely personal responsibility. The expectation that governments should manage crises and protect livelihoods took root.

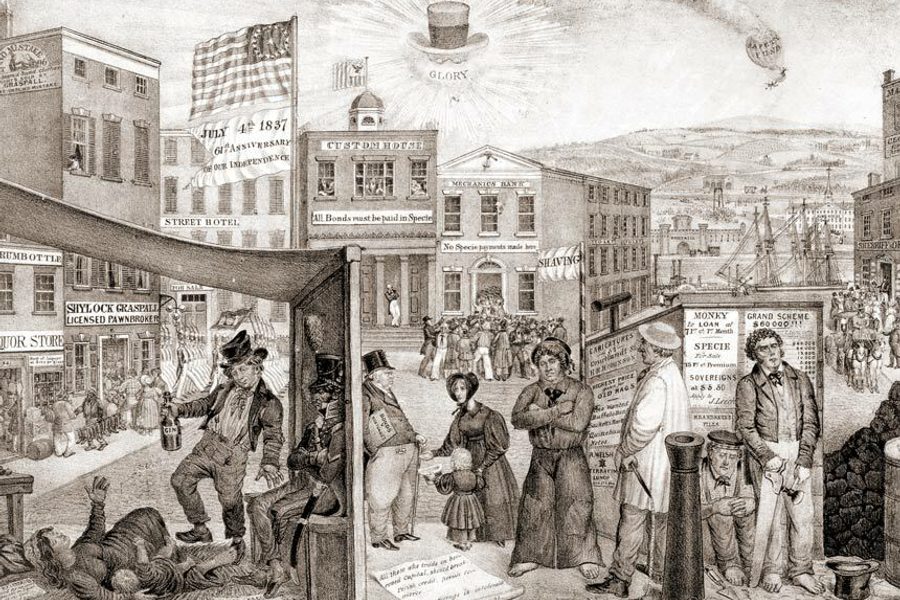

5. The Interwar Period: Instability, Protectionism, and Economic Breakdown

The years between the wars were economically chaotic. Attempts to return to pre-war systems failed.

Countries tried to restore the gold standard, but without the old balance of power, it created deflation and unemployment. War debts and reparations distorted trade. Nations turned inward, raising tariffs and restricting imports.

The Great Depression exposed how deeply fragile the global economy had become. International trade collapsed. Banking systems failed. Mass unemployment spread across industrialized nations.

These conditions did not just cause hardship — they fueled political extremism. Economic collapse made radical solutions attractive, directly shaping the path toward World War II.

6. World War II: Total Economic Transformation

If World War I introduced economic mobilization, World War II perfected it.

Entire national economies were redesigned around production efficiency. The scale was staggering:

-

Aircraft, tanks, ships, and weapons produced in the millions

-

Scientific research integrated directly into industry

-

Supply chains optimized across continents

Governments coordinated labor, capital, and technology with precision. In the United States, industrial output doubled. In the Soviet Union, factories were relocated across thousands of kilometers and resumed production under extreme conditions.

The war proved that economic power depended on industrial capacity, logistics, and technological innovation — not colonial territory alone.

7. The Rise of the United States as an Economic Superpower

World War II ended with the United States economically dominant in a way no nation had ever been.

Its homeland was untouched by destruction. Its factories were modernized. Its financial system was stable. It held the majority of the world’s gold reserves.

American companies expanded globally. The dollar became the anchor of international finance. U.S. economic influence replaced European imperial control in many regions.

This dominance was not accidental. It was built through wartime production, lending, and strategic planning.

8. Post-War Reconstruction and the Birth of a New Economic Order

When World War II ended, much of Europe and Asia lay physically and economically shattered. Cities were in ruins, industrial capacity destroyed, transportation networks broken, and populations displaced. Unlike after World War I, the response this time was deliberate, coordinated, and global in scale.

Reconstruction was not left to chance. Governments understood that economic collapse would invite political instability and future conflict. Massive rebuilding programs were launched to restore factories, housing, railways, and ports. Reconstruction was not just about returning to pre-war levels; it was about modernization. Old infrastructure was replaced with newer, more efficient systems, accelerating long-term growth.

This period also marked a shift in economic philosophy. Laissez-faire ideas lost credibility after the Depression and the war. Active government planning, public investment, and regulation were now seen as necessary tools for stability. The post-war world accepted that markets alone could not prevent collapse.

9. The Marshall Plan and the Logic of Economic Stability

One of the most influential economic interventions in history was the Marshall Plan. The United States provided vast financial aid to rebuild Western Europe, not as charity, but as strategy.

The logic was simple:

-

Economic recovery would prevent political extremism

-

Stable markets would support global trade

-

Prosperous allies would strengthen geopolitical security

Funds were used to rebuild industry, stabilize currencies, modernize agriculture, and restore confidence. Equally important, the program encouraged cooperation between European states, laying groundwork for future economic integration.

The Marshall Plan showed that economic policy could be a tool of global influence. Aid, investment, and trade replaced territorial conquest as instruments of power.

10. New Global Financial Institutions and Economic Governance

The World Wars exposed the dangers of uncoordinated national economies. In response, new international institutions were created to manage the global system.

The International Monetary Fund was designed to stabilize currencies and prevent destructive devaluations. The World Bank focused on reconstruction and development. Later, trade frameworks reduced tariffs and promoted international exchange.

These institutions reshaped how economies interacted. Economic crises were no longer purely national events; they became shared problems requiring coordinated solutions. This was a direct lesson from the interwar collapse.

For the first time, global economic governance existed as a permanent structure rather than an ad-hoc response.

11. The Transformation of Labor and the Middle Class

The World Wars fundamentally reshaped labor relations and social structure.

Wartime production strengthened unions and normalized collective bargaining. Governments accepted higher wages and worker protections as part of economic stability. After World War II, many countries expanded education, housing, and healthcare to support productive populations.

This led to the rapid expansion of the middle class in industrialized nations. Stable employment, rising wages, and consumer access created new domestic markets. Economic growth became linked to mass consumption rather than elite demand.

The idea that broad prosperity was essential for political stability became central to economic planning.

12. Decolonization and the Global Economic Shift

The wars weakened European empires beyond repair. Colonial powers emerged financially exhausted and politically constrained. At the same time, colonial populations had contributed soldiers, labor, and resources to the war effort, accelerating demands for independence.

Decolonization transformed the global economy. New nations entered international markets, often dependent on exporting raw materials while importing manufactured goods. This created new forms of economic inequality and dependency, replacing formal empire with economic influence.

Global trade expanded, but power remained uneven. The legacy of wartime extraction shaped development paths for decades.

13. Technology, Industry, and the War-Driven Acceleration of Growth

World Wars forced rapid technological advancement. Military necessity compressed decades of innovation into years.

Technologies developed or expanded during wartime included:

-

Mass production techniques

-

Aviation and aerospace

-

Electronics and computing

-

Chemical and pharmaceutical industries

After the wars, these technologies flowed into civilian economies, boosting productivity and creating entirely new industries. Economic growth increasingly depended on research, innovation, and skilled labor rather than raw materials alone.

The modern industrial economy was not a peacetime invention — it was forged under pressure.

14. Long-Term Global Inequality and Economic Realignment

While the World Wars produced growth in some regions, they deepened inequality elsewhere. Countries with intact infrastructure and capital surged ahead. Others struggled with debt, weak institutions, and limited industrial bases.

The global economy became more interconnected, but also more stratified. Financial power concentrated in fewer centers. Currency dominance replaced territorial control.

The wars did not create inequality, but they reshaped who benefited from the global system and who bore its costs.

15. How the World Wars Still Shape the Economy Today

Many features of the modern economy trace directly to wartime transformations:

-

Government responsibility for economic stability

-

Central banking and currency management

-

Military-industrial relationships

-

Global trade institutions

-

Strategic use of economic power

Even modern economic crises are managed using tools first normalized during wartime: stimulus spending, public debt, industrial coordination, and emergency intervention.

The World Wars forced humanity to confront the limits of unregulated systems. The global economy that emerged is imperfect, but it is consciously designed rather than accidental.

A World Rebuilt Through Conflict

The World Wars destroyed unimaginable wealth and lives, but they also dismantled outdated economic structures and forced the creation of new ones. The global economy today — interconnected, regulated, industrial, and financialized — is a direct outcome of those conflicts.

War did not simply interrupt economic history. It redirected it.